If you've had a newborn in the last eighteen months, you've probably heard the term "Trump Account" floating around this summer. Same if you're a grandparent, an aunt, an uncle, or the kind of family friend who shows up to first birthdays with a check in an envelope.

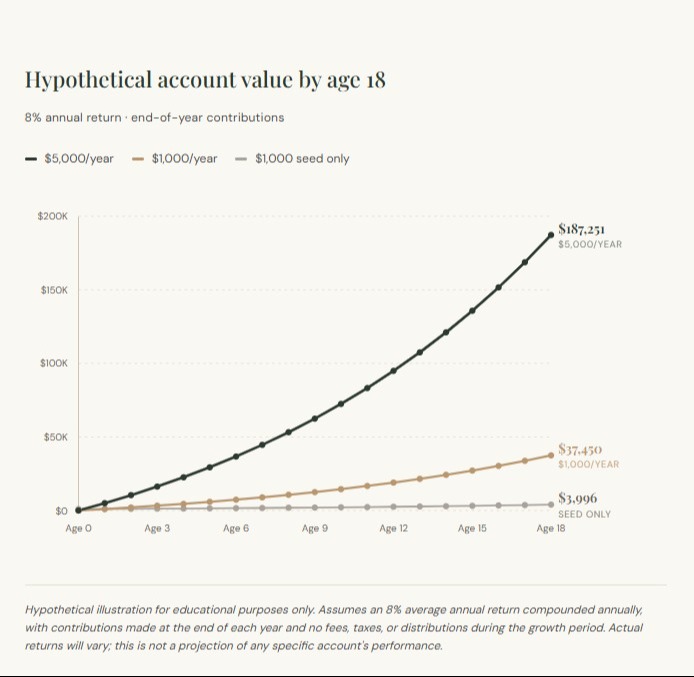

Before we get into the mechanics, here's what's at stake. Assuming an 8% average annual return, here's what a Trump Account could grow to by age 18:

Three very different outcomes. The government seed of $1,000 only grows to $4,000 after 18 years, with no other contributions. A steady $1,000 per year in contributions grows to roughly $37,000 by age 18, which is enough to make a real dent in a first apartment, a car, or a semester of graduate school.

Max the annual contribution of $5,000 a year, and the account lands at nearly $190,000 with an 8% annual return. That approximately $190,000 balance becomes the child's money at age 18, and they have full access to it at that time. Should they cash it out, or keep it invested? What happens with any taxes due if they take a withdrawal? Here's what these accounts actually are, where they belong in your family's plan, and where they probably don't.

What a Trump Account is (and isn't)

At the technical level, a Trump Account is a new type of Traditional IRA, set up on behalf of a child under 18. It was created by the One Big Beautiful Bill Act signed in 2025, and the first accounts became available for contributions on July 4, 2026.

Contributions during the "growth period" (birth through the year before the child turns 18) don't get you a tax deduction. But the money grows tax-deferred. On January 1 of the year the child turns 18, the account converts to a regular Traditional IRA, with the child in full legal control and standard IRA tax rules governing every withdrawal from that point forward.

Two features make Trump Accounts different from any other kid-focused savings vehicle:

- No earned income requirement. A Trump Account doesn't require the child to have any earned income at all. That's a real difference from a custodial Roth IRA, which many financial planners have championed for kids who work summer jobs.

- Others can contribute. Parents, grandparents, employers, state governments, and 501(c)(3) organizations can all put money in. There are coordination rules involved, which I'll cover below.

The $1,000 that has everyone's attention

The headline number that drove most of the coverage: a one-time $1,000 government contribution to every eligible child's Trump Account.

The catch is who's eligible:

- The child must be born between January 1, 2025 and December 31, 2028

- The child must be a U.S. citizen with a Social Security number

- A parent or guardian must actively elect the contribution. It's not automatic.

The election happens either through IRS Form 4547 on your tax return or through the online portal at trumpaccounts.gov. The Treasury Department will fund the $1,000 no earlier than July 4, 2026, and typically within a few months of a completed election.

The contribution rule that trips families up

Here's where I've already had a couple of client conversations that surprised me. The $5,000 annual contribution limit is combined across all individual sources.

Say Mom and Dad contribute $2,500. Then Grandma writes a $2,500 check at Christmas, and Grandpa on the other side does the same at New Year's. That's $7,500 into the account. You're now on the hook for a 6% excise tax on the $2,500 excess, every year, until it's withdrawn.

Employers can contribute up to $2,500 per year for their employees' children, but that $2,500 counts inside the $5,000 limit, not on top of it. So if your employer offers the benefit and contributes $2,500, the family can only contribute another $2,500 combined.

Where Trump Accounts fit, and where 529s still win

The most common question I've gotten so far is some version of: "Should we open a Trump Account instead of a 529?" For education savings specifically, the 529 is almost always the better tool.

What actually happens at 18

Come January 1 of the year the child turns 18, the Trump Account converts to a standard Traditional IRA. The child gains full legal control. The parent is no longer the responsible party and cannot block a withdrawal. If your now-adult child wants to empty the account on their 18th birthday, that is legally their call.

But "control" is not the same as "tax-free." From that point forward, standard Traditional IRA rules apply, which means every withdrawal is potentially subject to two taxes stacked on top of each other:

- Ordinary income tax on the taxable portion, at the child's marginal rate

- A 10% early withdrawal penalty on the taxable portion, if the child is under 59½ and no exception applies

What "taxable" means here

Not every dollar in the account is treated the same at withdrawal:

- Individual contributions from parents, grandparents, or other family members create basis in the account. They come back tax-free at withdrawal.

- The $1,000 government seed, employer contributions, philanthropic or state contributions, and all investment earnings don't create basis. They're 100% taxable as ordinary income when withdrawn.

And the pro-rata rule prevents cherry-picking. If your daughter withdraws $10,000 from an account that's 40% basis and 60% pre-tax, that withdrawal is treated as $4,000 tax-free basis and $6,000 taxable, regardless of what she says the money is for.

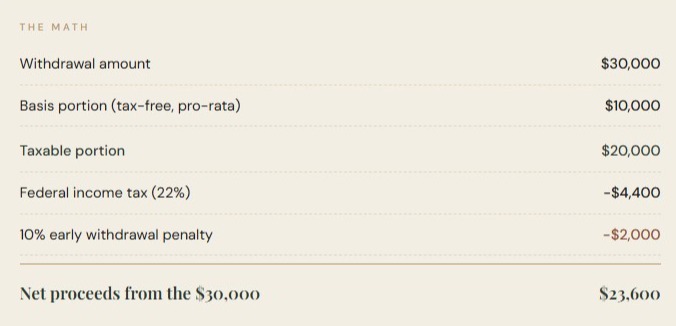

The math on a $30,000 car

Say your daughter turns 18 with a $150,000 Trump Account balance. Roughly one-third is basis (your and her grandparents' after-tax contributions), and two-thirds is pre-tax (the government seed, employer contributions, and all the compounded earnings). She's now 22, working her first job in a 22% federal bracket, and wants to pull $30,000 for a car.

She's given up more than 20% of the withdrawal to tax and penalty. And she's permanently removed $30,000 from an account that would have kept compounding tax-deferred for decades.

A favorable wrinkle for our Illinois clients: Illinois doesn't tax Traditional IRA distributions at all, even early ones subject to the federal penalty. That same withdrawal in California would add roughly $2,000 in state tax on top of the federal hit; in New York, closer to $1,300. Illinois residents get a clean federal-only calculation.

What if she leaves it alone instead?

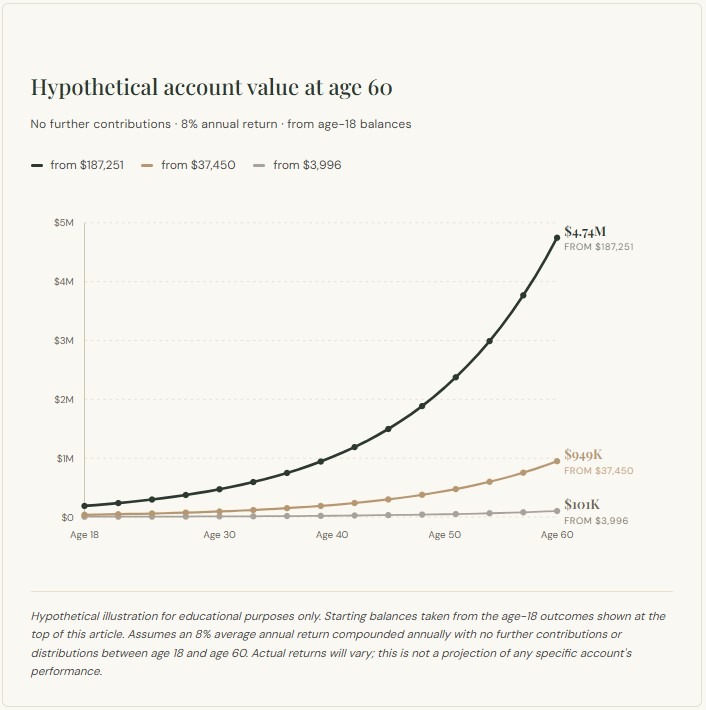

That $30,000 car withdrawal is one outcome. Here's the other. Remember the three age-18 balances from the chart at the top of this article: $3,996, $37,450, and $187,251. If your daughter keeps the account invested and makes no additional contributions, and lets those balances continue to grow at the same 8% assumed return until age 60 (when the 10% early withdrawal penalty stops applying entirely), the numbers change dramatically.

The seed-only path grows to roughly $101,000 by age 60. The $1,000-a-year path reaches nearly $950,000. And the maxed-out scenario compounds to almost $4.75 million, from a total of $90,000 in family contributions made during the first 18 years. Same account. Same 8% return. Wildly different outcomes based on whether the young adult treats it as a piggy bank at 18 or as the head start on retirement it was designed to be.

This is the case worth making to your future 18-year-old before they gain control of the account. The $30,000 they might pull for a car at 22 isn't just $30,000. At the same 8% return, that same $30,000 would have grown to nearly $560,000 by age 60.

The penalty-free exceptions

Standard Traditional IRA exceptions apply, which means some uses avoid the 10% penalty (income tax on the taxable portion still applies to all of them):

- Qualified higher education expenses (no dollar cap)

- First-time home purchase (up to $10,000 lifetime)

- Birth or adoption expenses (up to $5,000 per event)

- Qualified medical expenses, disability, terminal illness, and a handful of other narrower exceptions

The tax-and-penalty structure won't stop every impulsive teenager, but it does soften the concern families associate with UGMA/UTMA accounts. A Trump Account withdrawal for a car isn't the clean payday a UTMA would be. The friction is real, and it's designed to be.

One more thing worth having on the radar: Roth conversion

Once the account is a Traditional IRA, the young adult can convert some or all of it to a Roth IRA. The conversion triggers ordinary income tax at their current bracket, often 0-12% during their college years. But every dollar of future growth then compounds tax-free forever.

For families with a long runway, executing partial Roth conversions during a child's low-income years can turn a lifetime tax bill into something close to zero. That's a strategy that deserves its own article, and I'll write one. For now, it's enough to know that the Traditional IRA conversion at 18 is not the last opportunity to shape the account's tax profile. It's the beginning of the next one.

The wrinkles most articles are glossing over

A few planning details worth knowing before you open one:

Only your after-tax contributions create basis

Every dollar that comes in from the government seed, an employer, or a philanthropic organization is treated as pre-tax. That means it's fully taxable at withdrawal. Your personal contributions come back out tax-free at distribution, but the rest gets taxed as ordinary income. This is very different from a 529 or a Roth IRA and worth knowing before you assume "tax-advantaged" means "tax-free."

Investment options are limited

The account can only hold mutual funds or ETFs that track the S&P 500 or a similar index of primarily U.S. companies. That's more restrictive than a 529 (which offers age-based portfolios) or a Roth IRA (which offers whatever the custodian allows). For long-term growth purposes it's not a bad menu, but it's less flexible than most other kid-focused accounts.

Ask your employer about it

Employer contributions to Trump Accounts are a brand-new benefit category. Most employers haven't adopted them yet, but many are evaluating it, particularly larger companies looking for family-friendly benefits. If yours doesn't offer it, it's worth asking. And if you own a business, this is worth adding to the "should we offer it" list.

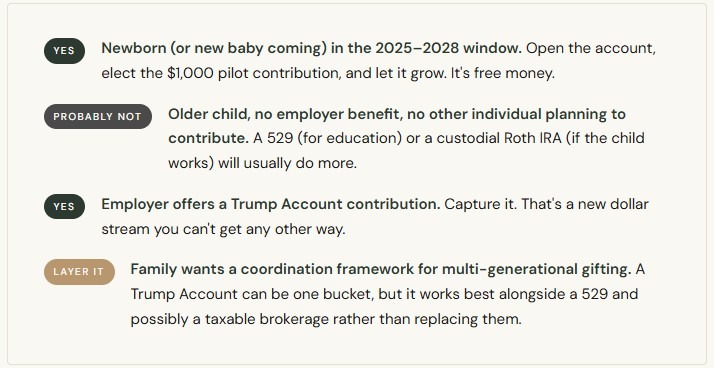

Should you open one?

The short version for most families I work with:

Not sure how this fits your family's plan?

The specifics change the answer. A grandparent looking to make a meaningful gift to a grandchild has different math than a working parent evaluating an employer benefit. If you'd like a second set of eyes on how a Trump Account fits alongside your family's 529, brokerage, or estate planning strategy, that's exactly the kind of thing we sort out together.

These examples are hypothetical only, and do not represent the actual performance of any particular investments. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and when sold or redeemed, you may receive more or less than originally invested.

Investors should consider the investment objectives, risks, charges and expenses associated with municipal fund securities before investing. This information is found in the issuer's official statement and should be read carefully before investing. Investors should also consider whether the investor’s or beneficiary’s home state offers any state tax or other benefits available only from that state’s 529 Plan. Any state-based benefit should be one of many appropriately weighted factors in making an investment decision. The investor should consult their financial or tax advisor before investment in any state's 529 Plan.

Converting from a traditional IRA to a Roth IRA is a taxable event. A Roth IRA offers tax free withdrawals on taxable contributions. To qualify for the tax-free and penalty-free withdrawal or earnings, a Roth IRA must be in place for at least five tax years, and the distribution must take place after age 59 ½ or due to death, disability, or a first-time home purchase (up to a $10,000 lifetime maximum). Depending on state law, Roth IRA distributions may be subject to state taxes.